Features

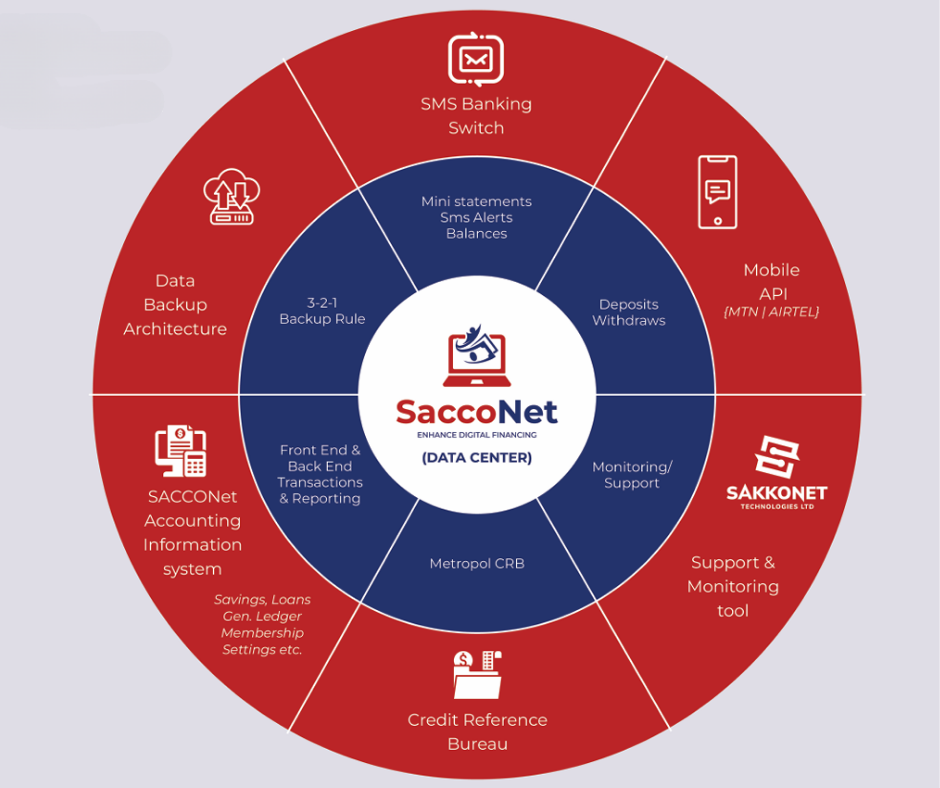

SaccoNet Core Banking Platform

CLOUD BASED BANKING SOLUTION

Provides standard accounting and reporting functionality for extraordinary organizational efficiency,

Improved risk management and additional income generation to the cooperative institution.

Our Application Features

1. CONFIGURATIONS MODULE

In this module, options and features that can be used to adapt SACCONET application to the requirements of any organization (microfinance organization) can be found. This module is used for System Configuration, System Administration and Users Management.

2. CUSTOMERS MODULE

SACCONET supports three major types of customers managed under the following menus: Individual Clients, Group Clients, Business Clients/Institutions. This module is used to track and manage customer features including Members registration, Modifying Members Details, Transfer Group members, Import membership data, Export membership data and Clients reports.

3. SHARES MODULE

The Shares module enables users to monitor all the shares transactions and dealings of the organization’s shareholders. This module is used to track and manage features including Buying of Shares, Transfer of Shares, Register of Current Share Value, Calculation of Dividends, Import Shares Transactions and Shares Reports.

4. SAVINGS MODULE

SACCONET tracks and manages the organization’s customers’ accounts. Savings Accounts are tracked based on designated savings products. Features include Open Savings Account, Deposits, Withdrawals, Importation, Charges and Rewards, Fixed Deposits, Overdrafts, Standing Orders and Savings Portfolio Reports.

5. CHART OF ACCOUNTS

SACCONET comes with a standard chart of accounts but this can be deleted or replaced by another chart. Accounts can be added, modified or deleted. Accounting data can also be exported to other third-party software.

6. LOANS MODULE

The Loans module is used to efficiently manage all loans transactions. Features include Loan Application, Approval/ Rejection, Disbursements, Repayments, Due Date Postponement, Interest Recalculation, Loan Importations, Penalties, Rescheduling, Write-offs, Portfolio Transfer, Updating Loan Categories, Guarantors, Collateral, Provision Calculation, and Loan Portfolio Reports.

7. CREDIT REFERENCE BUREAU (CRB)

This is a credit information and debt management bureau whose core activities are focused on the Credit and Capital Markets. It assesses the credit worthiness of borrowers through comprehensive Credit Scoring and Ratings and provides the resultant credit information reports to lenders and trade credit suppliers to enable them make sound credit decisions on their customers.

8. GL TRANSACTIONS MODULE

This module is used to post various General Ledger transactions and bookings to respective accounts. Features include Entering Manual Transactions, Modifying, Deleting, Reversing Transactions, Posting GL Opening balances and Importing Financial Transactions.

9. BOOK KEEPING MODULE

This module is used to Calculate Accrued Interest, perform Day/Month/Year Closures, Bank Accounts Reconciliation, Till Management, Budgeting, Assets Management, Purchases & Sales Management, and Financial & Regulatory Reporting.

Mobile Financial Services

SACCONET is integrated with MTN mobile money and Airtel Money to provide a convenient and effective solution for SACCOs to provide mobile financial services to their members.

Members can therefore make deposits and withdraw money from their respective accounts. This provides tremendous benefits both to the SACCO and members of the SACCO

Benefits of Mobile Finacial Services

To The SACCO Member

Convenience

Members transact from anywhere and at any time

Save Money and Time

Members don’t spend time and

money traveling to the banking hall any more.

Accountability

A member is in position to monitor the activities on

their accounts through mini statements.

Better Rating

Achieve a better Credit Rating by transacting more often

To The SACCO

Source of Income

A SACCO generates repetitive income from mobile banking transactions

Cheaper to do business

AS members no longer have to move to the banking halls, there is no need for setting up multiple banking halls/outreach.

Customer Retention

Regardless of which town, village or district in Uganda a member shifts to, members can be served via their phones

Automation Process

For quick automation of an institution (SACCO or MFI), a chronological step by step process is proposed to achieve desired goals. Below are the six (6) technical stages that chronologically evolve to successfully automate a SACCO or microfinance institution

DATA COLLECTION AND ORGANIZATION’S OPERATING REQUIREMENTS GATHERING

UCCFS deploys an accounting team to collect data (Savings balances, shares balances, outstanding loans and trial balances). The team also collects all operating requirements for the SACCO to be configured on the SACCO’s instance.

DATABASE IMPLEMENTATION AND CONFIGURATION

Data and requirements from stage 1 are submitted to UCCFS technical team for database installation, data migration and configuring the SACCO’s system to meet its operating requirements.

AGGREGATED SYSTEM USERS’ (STAFF AND BOARD) TRAINING

Trainers explain MOU obligations and train staff and board members in basic computer and network literacy. Later, they are trained on using SACCONET for their specific tasks.

LAN INSTALLATION AND USERS’ ACCEPTANCE TESTING

A LAN is set up to connect devices to SACCONET. Backlog data is posted, users interact with the system, and generate reports to confirm correctness.

SYSTEM MONITORING AND SUPPORT

The DIFICO II project provides one year free onsite and online support to ensure maximum efficiency in SACCO operations.

MOBILE BANKING INTEGRATION

On successful mobile banking integration, SACCO management submits KYC forms to MTN and Airtel to acquire SACCO IDs for members’ transactions.